This hearing, entitled "Fractional Reserve Banking and the Federal Reserve: The Economic Consequences of High-Powered Money," will be held on Thursday, June 28, at 2:00 p.m. in room 2128 of the Rayburn House Office Building.

Witnesses scheduled to testify:

Dr. John Cochran, Emeritus Professor of Economics and Emeritus Dean, School of Business, Metropolitan State College of Denver Dr. Joseph Salerno, Professor of Economics, Lubin School of Business, Pace University Dr. Lawrence H. White, Professors of Economics, George Mason University

"Fractional reserve banking underpins the entire banking system, yet its effects on society are completely ignored. Our financial system consists of vast amounts of credit pyramided on top of very small amounts of real savings-- all backstopped by explicit and implicit government guarantees. This poses significant risks to the stability of the economy and monetary system, which ought to give pause to any serious observer of financial markets. Hopefully this hearing will create a greater understanding among the American people about the nature of the banking system, and begin the movement towards serious systematic reform. The American people deserve a financial system that is stable and efficient; one that operates without taxpayer subsidies and bailouts." - Congressman Ron Paul

Hearing June 28 2012 Fractional Reserve Banking

Saturday, June 30, 2012

Friday, June 29, 2012

Do We Really Need a Central Bank? | Steven Horwitz

Steven Horwitz gave this lecture entitled "Do We Really Need a Central Bank?" at the Future of Freedom Foundation's Economic Liberty Lecture Series at George Mason University on December 2, 2009.

Steven Horwitz is the Charles A. Dana Professor of Economics at St. Lawrence University in Canton, NY. He is the author of two books, Microfoundations and Macroeconomics: An Austrian Perspective (Routledge, 2000) and Monetary Evolution, Free Banking, and Economic Order (Westview, 1992), and he has written extensively on Austrian economics, Hayekian political economy, monetary theory and history, and the economics and social theory of gender and the family.

His work has been published in professional journals such as History of Political Economy, Southern Economic Journal, and The Cambridge Journal of Economics. He has also done public policy research for the Mercatus Center, Heartland Institute, Citizens for a Sound Economy, and the Cato Institute. His current project is a book tentatively titled Classical Liberalism and the Evolution of the Modern Family. Horwitz currently serves as the book review editor of The Review of Austrian Economics and as an academic advisor for the Heartland Institute and a contributing editor to Critical Review and Journal des Economistes et des Etudes Humaines. A member of the Mont Pelerin Society, he completed his MA and PhD in economics at George Mason University and received his A.B. in economics and philosophy from The University of Michigan.

Steven Horwitz at FFF: "Do We Really Need a Central Bank?"

Steven Horwitz is the Charles A. Dana Professor of Economics at St. Lawrence University in Canton, NY. He is the author of two books, Microfoundations and Macroeconomics: An Austrian Perspective (Routledge, 2000) and Monetary Evolution, Free Banking, and Economic Order (Westview, 1992), and he has written extensively on Austrian economics, Hayekian political economy, monetary theory and history, and the economics and social theory of gender and the family.

His work has been published in professional journals such as History of Political Economy, Southern Economic Journal, and The Cambridge Journal of Economics. He has also done public policy research for the Mercatus Center, Heartland Institute, Citizens for a Sound Economy, and the Cato Institute. His current project is a book tentatively titled Classical Liberalism and the Evolution of the Modern Family. Horwitz currently serves as the book review editor of The Review of Austrian Economics and as an academic advisor for the Heartland Institute and a contributing editor to Critical Review and Journal des Economistes et des Etudes Humaines. A member of the Mont Pelerin Society, he completed his MA and PhD in economics at George Mason University and received his A.B. in economics and philosophy from The University of Michigan.

Steven Horwitz at FFF: "Do We Really Need a Central Bank?"

MUST WATCH! Four Principles for the Open World | Don Tapscott [TED]

The recent generations have been bathed in connecting technology from birth, says futurist Don Tapscott, and as a result the world is transforming into one that is far more open and transparent. In this inspiring talk, he lists the four core principles that show how this open world can be a far better place.

Don Tapscott: Four principles for the open world

Don Tapscott: Four principles for the open world

MUST READ! A Conversation With Bill Gates About the Future of Higher Education

Bill Gates never finished college, but he is one of the single most powerful figures shaping higher education today. That influence comes through the Bill & Melinda Gates Foundation, perhaps the world's richest philanthropy, which he co-chairs and which has made education one of its key missions.

The Chronicle sat down with Mr. Gates in an exclusive interview Monday to talk about his vision for how colleges can be transformed through technology. His approach is not simply to drop in tablet computers or other gadgets and hope change happens—a model he said has a "really horrible track record." Instead, the foundation awards grants to reformers working to fix "inefficiencies" in the current model of higher education that keep many students from graduating on time, or at all. And he argues for radical reform of college teaching, advocating a move toward a "flipped" classroom, where students watch videos from superstar professors as homework and use class time for group projects and other interactive activities. As he put it, "having a lot of kids sit in the lecture class will be viewed at some point as an antiquated thing."

The Microsoft founder doesn't claim to have all the answers. In fact, he describes the foundation's process as one of continual refinement: "to learn, make mistakes, try new things out, find new partners to do things."

The interview comes on the eve of Mr. Gates's keynote speech at an event Tuesday to celebrate the 150th anniversary of the Morrill Act, which created the nationwide system of land-grant colleges. The "convocation" will be held in Washington, D.C., sponsored by the Association of Public Land-Grant Universities.

Q. You have been interested in education for quite a while. I was looking back at your 1995 book, The Road Ahead, and you laid out a vision of education and how it could be transformed with technology. It seems like some of that vision is still only just emerging, so many years later. Did it take longer than you thought it would?

A. Oh sure. Education has not been changed. That is, institutional education, whether it's K-12 or higher education, has not been substantially changed by the Internet. And we've seen that with other waves of technology. Where we had broadcast TV people thought would change things. We had early time-sharing computing—so-called CAI, computer-assisted instruction—where people could do these drills, and people thought that would change things. So it's easy to say that people have been overoptimistic in the past. But I think this wave is quite different. I think it's more fundamental. And we can say that individual education has changed. That is, for the highly-motivated student, the ability to go online and find lectures of various length—to see class materials—there's a lot of people who are learning far better because of those materials. But it's much harder to then take it for the broad set of students in the institutional framework and decide, OK, where is technology the best and where is the face-to-face the best. And they don't have very good metrics of what is their value-added. If you try and compare two universities, you'll find out a lot more about the inputs—this university has high SAT scores compared to this one. And it's sort of the opposite of what you'd think. You'd think people would say, "We take people with low SATs and make them really good lawyers." Instead they say, "We take people with very high SATs and we don't really know what we create, but at least they're smart when they show up here so maybe they still are when we're done with them." So it's a field without a kind of clear metric that then you can experiment and see if you're still continuing to achieve it.

Q. So who's to blame? Are there things like the U.S. News rankings or other pressures that give colleges the wrong incentives?

A. Well there certainly is a perverse set of incentives to a lot of universities to compete for the best students. And whether that comes out in terms of being more selective or investing in sort of the living experience, it's probably not where you'd like the innovation and energy to go. You'd like it to go into the completion rates, the quality of the employees that get generated by the learning experience. The various rankings have focused on the input side of the equation, not the output.

Q. There's a moving moment in Walter Isaacson's biography of Steve Jobs that describes a time when you visited Mr. Jobs at his house not long before his passing, and the two you reflected on the innovations you both led in technology. I understand that one thing Steve Jobs asked you that day was about how technology could change education. What did you tell him?

A. Well, I'd been involved in the education space because of my full-time foundation work. And so I'd been able to get out to various charter schools, to inner-city high schools, to community colleges, different universities, and learn about the financial situation about what discourages kids. And based on that, you get more of a sense of, OK where can technology come in? If the kids don't have to come to the campus quite as often, that would be good. But then what's the element that technology can't deliver? And it's through that that I really have developed a lot of optimism that we can build a hybrid. Something that's not purely digital but also that the efficiency of the face-to-face time is much greater. Where you take the kid who's demotivated or confused, or where something needs to be a group collaboration as opposed to the lecture. So I talked about the vision and what type of innovators we should draw in.

Q. Getting to some of those ideas, you're famously not a college graduate, since you left Harvard early to start Microsoft. So I'm curious what you think of EdX out of Harvard and MIT. What do you think of that model of certificates or badges for taking free online courses?

A. Well at the end of the day you've got to have something that employers really believe in. And today what they believe in by and large are degrees. And if you have a great degree then you're considered for jobs, and if you don't have that degree there's a lot of jobs you won't get consideration for. And so the question is, Can we transform this credentialing process? And in fact the ideal would be to separate out the idea of proving your knowledge from the way you acquire that knowledge. So even though I only have a high-school degree, I am a professional student. That is, I like to watch courses and do things online. So things like OpenCourseWare, the various lectures that have been put online, I consume a lot of those because I'm very interested.

Continue reading - A Conversation With Bill Gates About the Future of Higher Education

On Business's Role in Higher Education

On Tablets in the Classroom

On the Meaning of MOOC's

On the Role of Technology in Academe

On the Future of His Foundation

On the Future of ‘Place-Based’ Colleges

On Why There Won’t Be a Gates U.

The Chronicle sat down with Mr. Gates in an exclusive interview Monday to talk about his vision for how colleges can be transformed through technology. His approach is not simply to drop in tablet computers or other gadgets and hope change happens—a model he said has a "really horrible track record." Instead, the foundation awards grants to reformers working to fix "inefficiencies" in the current model of higher education that keep many students from graduating on time, or at all. And he argues for radical reform of college teaching, advocating a move toward a "flipped" classroom, where students watch videos from superstar professors as homework and use class time for group projects and other interactive activities. As he put it, "having a lot of kids sit in the lecture class will be viewed at some point as an antiquated thing."

The Microsoft founder doesn't claim to have all the answers. In fact, he describes the foundation's process as one of continual refinement: "to learn, make mistakes, try new things out, find new partners to do things."

The interview comes on the eve of Mr. Gates's keynote speech at an event Tuesday to celebrate the 150th anniversary of the Morrill Act, which created the nationwide system of land-grant colleges. The "convocation" will be held in Washington, D.C., sponsored by the Association of Public Land-Grant Universities.

Q. You have been interested in education for quite a while. I was looking back at your 1995 book, The Road Ahead, and you laid out a vision of education and how it could be transformed with technology. It seems like some of that vision is still only just emerging, so many years later. Did it take longer than you thought it would?

A. Oh sure. Education has not been changed. That is, institutional education, whether it's K-12 or higher education, has not been substantially changed by the Internet. And we've seen that with other waves of technology. Where we had broadcast TV people thought would change things. We had early time-sharing computing—so-called CAI, computer-assisted instruction—where people could do these drills, and people thought that would change things. So it's easy to say that people have been overoptimistic in the past. But I think this wave is quite different. I think it's more fundamental. And we can say that individual education has changed. That is, for the highly-motivated student, the ability to go online and find lectures of various length—to see class materials—there's a lot of people who are learning far better because of those materials. But it's much harder to then take it for the broad set of students in the institutional framework and decide, OK, where is technology the best and where is the face-to-face the best. And they don't have very good metrics of what is their value-added. If you try and compare two universities, you'll find out a lot more about the inputs—this university has high SAT scores compared to this one. And it's sort of the opposite of what you'd think. You'd think people would say, "We take people with low SATs and make them really good lawyers." Instead they say, "We take people with very high SATs and we don't really know what we create, but at least they're smart when they show up here so maybe they still are when we're done with them." So it's a field without a kind of clear metric that then you can experiment and see if you're still continuing to achieve it.

Q. So who's to blame? Are there things like the U.S. News rankings or other pressures that give colleges the wrong incentives?

A. Well there certainly is a perverse set of incentives to a lot of universities to compete for the best students. And whether that comes out in terms of being more selective or investing in sort of the living experience, it's probably not where you'd like the innovation and energy to go. You'd like it to go into the completion rates, the quality of the employees that get generated by the learning experience. The various rankings have focused on the input side of the equation, not the output.

Q. There's a moving moment in Walter Isaacson's biography of Steve Jobs that describes a time when you visited Mr. Jobs at his house not long before his passing, and the two you reflected on the innovations you both led in technology. I understand that one thing Steve Jobs asked you that day was about how technology could change education. What did you tell him?

A. Well, I'd been involved in the education space because of my full-time foundation work. And so I'd been able to get out to various charter schools, to inner-city high schools, to community colleges, different universities, and learn about the financial situation about what discourages kids. And based on that, you get more of a sense of, OK where can technology come in? If the kids don't have to come to the campus quite as often, that would be good. But then what's the element that technology can't deliver? And it's through that that I really have developed a lot of optimism that we can build a hybrid. Something that's not purely digital but also that the efficiency of the face-to-face time is much greater. Where you take the kid who's demotivated or confused, or where something needs to be a group collaboration as opposed to the lecture. So I talked about the vision and what type of innovators we should draw in.

Q. Getting to some of those ideas, you're famously not a college graduate, since you left Harvard early to start Microsoft. So I'm curious what you think of EdX out of Harvard and MIT. What do you think of that model of certificates or badges for taking free online courses?

A. Well at the end of the day you've got to have something that employers really believe in. And today what they believe in by and large are degrees. And if you have a great degree then you're considered for jobs, and if you don't have that degree there's a lot of jobs you won't get consideration for. And so the question is, Can we transform this credentialing process? And in fact the ideal would be to separate out the idea of proving your knowledge from the way you acquire that knowledge. So even though I only have a high-school degree, I am a professional student. That is, I like to watch courses and do things online. So things like OpenCourseWare, the various lectures that have been put online, I consume a lot of those because I'm very interested.

Continue reading - A Conversation With Bill Gates About the Future of Higher Education

On Business's Role in Higher Education

On Tablets in the Classroom

On the Meaning of MOOC's

On the Role of Technology in Academe

On the Future of His Foundation

On the Future of ‘Place-Based’ Colleges

On Why There Won’t Be a Gates U.

Thursday, June 28, 2012

How Arduino Is Open-Sourcing Imagination | Massimo Banzi [TED]

Massimo Banzi helped invent the Arduino, a tiny, easy-to-use open-source microcontroller that's inspired thousands of people around the world to make the coolest things they can imagine -- from toys to satellite gear. Because, as he says, "You don't need anyone's permission to make something great."

Massimo Banzi: How Arduino is open-sourcing imagination

Massimo Banzi: How Arduino is open-sourcing imagination

Amazing Google Glasses Demonstration at Google I/O 2012 | Project Glass

Google Glasses Live Demonstration - During the Google I/O 2012 keynote, the audience was about to experience an amazing demonstration of Google Glasses.

Amazing Google Glasses Demonstration at Google I/O 2012

Amazing Google Glasses Demonstration at Google I/O 2012

Monday, June 25, 2012

Driving Innovation & Breakthroughs | Peter Diamandis | Singularity University

Peter Diamandis shares his insights on exponentially growing technologies.

Abundance - Peter Diamandis

Extra: At Singularity University: World's biggest problems also biggest market opportunities

Abundance - Peter Diamandis

Extra: At Singularity University: World's biggest problems also biggest market opportunities

A New Type of Mathematics | David Dalrymple [TEDx]

Accepted to MIT graduate school at 14 years old — the youngest ever — David Dalrymple will share his deep insight into the future of mathematics.

TEDxMontreal - David Dalrymple - A new type of mathematics

TEDxMontreal - David Dalrymple - A new type of mathematics

MIND-BLOWING SPEECH! Victoria Grant, a 12-year old girl, Explains The Banking System

12-year old Victoria Grant explains why her homeland, Canada, and most of the world, is in debt. April 27, 2012 at the Public Banking in America Conference, Philadelphia, PA.

Victoria Grant

Victoria Grant

THE PRICE OF INEQUALITY: How Today's Divided Society Endangers Our Future | Joseph Stiglitz

Joseph Stiglitz, Nobel Memorial Prize in Economic Sciences recipient (2001) , visited Google on June 12, 2012 to talk about his new book THE PRICE OF INEQUALITY: How Today's Divided Society Endangers Our Future.

The 1 Percent's Problem

"Why won't America's 1 percent—such as the six Walmart heirs, whose wealth equals that of the entire bottom 30 percent—be a bit more . . . selfish? As the widening financial divide cripples the U.S. economy, even those at the top will pay a steep price."

Authors@Google: Joseph Stiglitz

The 1 Percent's Problem

"Why won't America's 1 percent—such as the six Walmart heirs, whose wealth equals that of the entire bottom 30 percent—be a bit more . . . selfish? As the widening financial divide cripples the U.S. economy, even those at the top will pay a steep price."

Authors@Google: Joseph Stiglitz

Out-of Body Experiences, Consciousness, and Cognitive Neuroprosthetics | Olaf Blanke [TEDx]

What is a conscious self ? What exactly makes an experience a subjective phenomenon ?

Starting with the neurology of out-of-body experiences and the breakdown of bodily mechanisms of self-consciousness, this talk presents novel neuroscience data on selfconsciousness and subjectivity in healthy subjects using techniques from cognitive neuroscience and engineering-based technologies such as virtual reality and robotics. It translates these research findings to the bedside and show how control over the brain mechanisms of our daily "inside--body experience" can join forces with neuro-engineering and thus impact treatments for patients with amputation and spinal cord injury.

Olaf Blanke is director of the Center for Neuroprosthetics at the Ecole Polytechnique Fédérale de Lausanne (EPFL), holds the Bertarelli Foundation Chair in Cognitive Neuroprosthetics, and is consultant neurologist at the Department of Neurology (Geneva University Hospital). He received his MD and PhD in neurophysiology from the Free University of Berlin. Blanke's research targets the brain mechanisms of body perception, corporeal awareness and selfconsciousness, applying paradigms from cognitive science, neuroscience, neuroimaging, robotics, and virtual reality in healthy subjects and neurological patients. His two main goals are to understand and control neural own body representations to develop a neurobiological model of self-consciousness and to apply these findings in the emerging field of cognitive and systems neuroprosthetics. His work has received wide press coverage; he is recipient of numerous awards.

TEDxCHUV - Olaf Blanke - Out-of Body Experiences, Consciousness, and Cognitive Neuroprosthetics

Starting with the neurology of out-of-body experiences and the breakdown of bodily mechanisms of self-consciousness, this talk presents novel neuroscience data on selfconsciousness and subjectivity in healthy subjects using techniques from cognitive neuroscience and engineering-based technologies such as virtual reality and robotics. It translates these research findings to the bedside and show how control over the brain mechanisms of our daily "inside--body experience" can join forces with neuro-engineering and thus impact treatments for patients with amputation and spinal cord injury.

Olaf Blanke is director of the Center for Neuroprosthetics at the Ecole Polytechnique Fédérale de Lausanne (EPFL), holds the Bertarelli Foundation Chair in Cognitive Neuroprosthetics, and is consultant neurologist at the Department of Neurology (Geneva University Hospital). He received his MD and PhD in neurophysiology from the Free University of Berlin. Blanke's research targets the brain mechanisms of body perception, corporeal awareness and selfconsciousness, applying paradigms from cognitive science, neuroscience, neuroimaging, robotics, and virtual reality in healthy subjects and neurological patients. His two main goals are to understand and control neural own body representations to develop a neurobiological model of self-consciousness and to apply these findings in the emerging field of cognitive and systems neuroprosthetics. His work has received wide press coverage; he is recipient of numerous awards.

TEDxCHUV - Olaf Blanke - Out-of Body Experiences, Consciousness, and Cognitive Neuroprosthetics

Understanding the Human Brain: A Test of Global Collaboration | Henry Markram [TEDx]

Knowledge of the brain is highly fragmented and we have no way to prioritize the many experiments needed to fill the gaps in our understanding. It is time for a strategy of global collaboration, where scientists of all disciplines work together to solve this problem. We propose building a platform to catalyze efforts, integrate knowledge, and use supercomputers to simulate what is known about the brain, to predict gaps in our knowledge of the brain, and to test hypotheses about how it works.

Henry Markram is the Coordinator of the Human Brain Project, a proposed international effort to understand the human brain. His research career started in medicine and neuroscience in South Africa, then at the Weizmann Institute in Israel, at NIH and UCSF in the United States, and the Max-Planck Institute in Germany. In 2002, he joined the EPFL, where he founded the Brain Mind Institute. His career has spanned a wide spectrum of neuroscience research, from whole animal studies to gene expression in single cells. He is best known for his work on synaptic plasticity. In the past 15 years he has focused on the structure and function of neural microcircuits -- the basic components in the architecture of the brain. In 2005, he launched the Blue Brain Project: the first attempt to begin a systematic integration of all biological knowledge of the brain into unifying brain models for simulation on supercomputers. The strategies, technologies and methods developed in this pioneering work lie at the heart of the Human Brain Project.

TEDxCHUV - Henry Markram - Understanding the Human Brain: a test of global collaboration

Henry Markram is the Coordinator of the Human Brain Project, a proposed international effort to understand the human brain. His research career started in medicine and neuroscience in South Africa, then at the Weizmann Institute in Israel, at NIH and UCSF in the United States, and the Max-Planck Institute in Germany. In 2002, he joined the EPFL, where he founded the Brain Mind Institute. His career has spanned a wide spectrum of neuroscience research, from whole animal studies to gene expression in single cells. He is best known for his work on synaptic plasticity. In the past 15 years he has focused on the structure and function of neural microcircuits -- the basic components in the architecture of the brain. In 2005, he launched the Blue Brain Project: the first attempt to begin a systematic integration of all biological knowledge of the brain into unifying brain models for simulation on supercomputers. The strategies, technologies and methods developed in this pioneering work lie at the heart of the Human Brain Project.

TEDxCHUV - Henry Markram - Understanding the Human Brain: a test of global collaboration

Sunday, June 24, 2012

MUST WATCH! Medicine's Future? There's An App For That | Daniel Kraft [TEDx]

At TEDxMaastricht, Daniel Kraft offers a fast-paced look at the next few years of innovations in medicine, powered by new tools, tests and apps that bring diagnostic information right to the patient's bedside.

Daniel Kraft: Medicine's future? There's an app for that

Daniel Kraft: Medicine's future? There's an app for that

Saturday, June 23, 2012

Quantum Computation | Michelle Simmons [TEDx]

There is a shift coming in the very nature of computing which is being led by the likes of quantum physicist Michelle Simmons. Michelle wants you to put the binary world of ones and zeros on the shelf for a moment, as she introduces you to the idea of computing with atoms.

Michelle has always wanted to undertake the hardest research in the hardest subject: quantum physics. Her eccentric schooling, coupled with the sudden death of her PhD supervisor means she has spent most of her career teaching herself. Michelle is the Director of Australia's Centre of Excellence for Quantum Computation and Communication Technology. This year, she and her team announced they had made the first ever single atom transistor. They now sit on the threshold of delivering the first ever quantum computer to the world.

TEDxSydney - Professor Michelle Simmons -- Quantum Computation

Michelle has always wanted to undertake the hardest research in the hardest subject: quantum physics. Her eccentric schooling, coupled with the sudden death of her PhD supervisor means she has spent most of her career teaching herself. Michelle is the Director of Australia's Centre of Excellence for Quantum Computation and Communication Technology. This year, she and her team announced they had made the first ever single atom transistor. They now sit on the threshold of delivering the first ever quantum computer to the world.

TEDxSydney - Professor Michelle Simmons -- Quantum Computation

Friday, June 22, 2012

MUST READ! The Scam Wall Street Learned From the Mafia | Matt Taibbi

Someday, it will go down in history as the first trial of the modern American mafia. Of course, you won't hear the recent financial corruption case, United States of America v. Carollo, Goldberg and Grimm, called anything like that. If you heard about it at all, you're probably either in the municipal bond business or married to an antitrust lawyer. Even then, all you probably heard was that a threesome of bit players on Wall Street got convicted of obscure antitrust violations in one of the most inscrutable, jargon-packed legal snoozefests since the government's massive case against Microsoft in the Nineties – not exactly the thrilling courtroom drama offered by the famed trials of old-school mobsters like Al Capone or Anthony "Tony Ducks" Corallo.

But this just-completed trial in downtown New York against three faceless financial executives really was historic. Over 10 years in the making, the case allowed federal prosecutors to make public for the first time the astonishing inner workings of the reigning American crime syndicate, which now operates not out of Little Italy and Las Vegas, but out of Wall Street.

The defendants in the case – Dominick Carollo, Steven Goldberg and Peter Grimm – worked for GE Capital, the finance arm of General Electric. Along with virtually every major bank and finance company on Wall Street – not just GE, but J.P. Morgan Chase, Bank of America, UBS, Lehman Brothers, Bear Stearns, Wachovia and more – these three Wall Street wiseguys spent the past decade taking part in a breathtakingly broad scheme to skim billions of dollars from the coffers of cities and small towns across America. The banks achieved this gigantic rip-off by secretly colluding to rig the public bids on municipal bonds, a business worth $3.7 trillion. By conspiring to lower the interest rates that towns earn on these investments, the banks systematically stole from schools, hospitals, libraries and nursing homes – from "virtually every state, district and territory in the United States," according to one settlement. And they did it so cleverly that the victims never even knew they were being cheated. No thumbs were broken, and nobody ended up in a landfill in New Jersey, but money disappeared, lots and lots of it, and its manner of disappearance had a familiar name: organized crime.

In fact, stripped of all the camouflaging financial verbiage, the crimes the defendants and their co-conspirators committed were virtually indistinguishable from the kind of thuggery practiced for decades by the Mafia, which has long made manipulation of public bids for things like garbage collection and construction contracts a cornerstone of its business. What's more, in the manner of old mob trials, Wall Street's secret machinations were revealed during the Carollo trial through crackling wiretap recordings and the lurid testimony of cooperating witnesses, who came into court with bowed heads, pointing fingers at their accomplices. The new-age gangsters even invented an elaborate code to hide their crimes. Like Elizabethan highway robbers who spoke in thieves' cant, or Italian mobsters who talked about "getting a button man to clip the capo," on tape after tape these Wall Street crooks coughed up phrases like "pull a nickel out" or "get to the right level" or "you're hanging out there" – all code words used to manipulate the interest rates on municipal bonds. The only thing that made this trial different from a typical mob trial was the scale of the crime.

USA v. Carollo involved classic cartel activity: not just one corrupt bank, but many, all acting in careful concert against the public interest. In the years since the economic crash of 2008, we've seen numerous hints that such orchestrated corruption exists. The collapses of Bear Stearns and Lehman Brothers, for instance, both pointed to coordinated attacks by powerful banks and hedge funds determined to speed the demise of those firms. In the bankruptcy of Jefferson County, Alabama, we learned that Goldman Sachs accepted a $3 million bribe from J.P. Morgan Chase to permit Chase to serve as the sole provider of toxic swap deals to the rubes running metropolitan Birmingham – "an open-and-shut case of anti-competitive behavior," as one former regulator described it.

More recently, a major international investigation has been launched into the manipulation of Libor, the interbank lending index that is used to calculate global interest rates for products worth more than $3 trillion a year. If and when that case is presented to the public at trial – there are several major civil suits in the works here in the States – we may yet find out that the world's most powerful banks have, for years, been fixing the prices of almost every adjustable-rate vehicle on earth, from mortgages and credit cards to interest-rate swaps and even currencies.

But USA v. Carollo marks the first time we actually got incontrovertible evidence that Wall Street has moved into this cartel-type brand of criminality. It also offered a disgusting glimpse into the enabling and grossly cynical role played by politicians, who took Super Bowl tickets and bribe-stuffed envelopes to look the other way while gangsters raided the public kitty. And though the punishments that were ultimately handed down in the trial – minor convictions of three bit players – felt deeply unsatisfying, it was still a watershed moment in the ongoing story of America's gradual awakening to the realities of financial corruption. In a post-crash era where Wall Street trials almost never make it into court, and even the harshest settlements end with the evidence buried by the government and the offending banks permitted to escape with no admission of wrongdoing, this case finally dragged the whole ugly truth of American finance out into the open – and it was a hell of a show.

1. THE SCAM

This was no trial scene from popular lore, no Inherit the Wind or State of California v. Orenthal James Simpson. No gallery packed with rapt spectators, no ceiling fans set whirring to beat back the tension and the heat, no defense counsel's resting a sympathetic hand on the defendant's shoulder as opening statements commence. No, the setting for USA v. Carollo reflected the bizarre alternate universe that exists on Wall Street. Like so many court cases involving big banks, the proceeding looked more like a roomful of expensive lawyers negotiating a major corporate merger than a public search for justice.

The trial began on April 16th in a federal court in Lower Manhattan. The courtroom, an aerielike setting 23 stories up, offered a panoramic view of the city and the East River. Though the gallery was usually full throughout the three-plus weeks of testimony, the spectators were not average citizens come to witness how they had been robbed blind by America's biggest banks. Instead, there were row after row of suits – other lawyers eager to observe a long-awaited case, one that could influence the outcome in a handful of civil suits pending across the country. In fact, the defendants themselves, whom the trial would reveal as easily replaceable cogs in a much larger machine of corruption, were barely visible from the gallery, obscured by the great chattering congress of prosecution and defense attorneys.

Only the presence of the mostly nonwhite and elderly jury, which resembled the front pew of a Harlem church, served as a reminder that the case had any connection to the real world. Even reporters from most of the major news outlets didn't bother to attend. The judge in the trial, the right honorable and amusingly cantankerous Harold Baer, acknowledged that the case was not likely to set the public's pulse racing. "It is unlikely, I think, that this will generate a lot of media publicity," Baer sighed to the jury in his preliminary instructions.

Continue reading (Long read) - The Scam Wall Street Learned From the Mafia

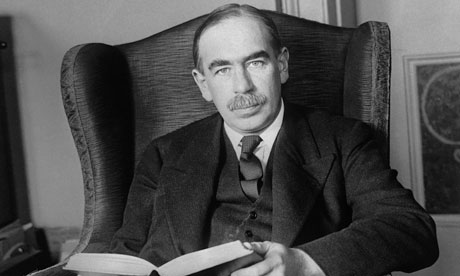

Labor’s Paradise Lost | Robert Skidelsky | Technological Unemployment

As people in the developed world wonder how their countries will return to full employment after the global recession, it might benefit us to take a look at a visionary essay that John Maynard Keynes wrote in 1930, called Economic Possibilities for our Grandchildren.

Keynes's General Theory of Employment, Interest, and Money, published in 1936, equipped governments with the intellectual tools to counter the unemployment caused by slumps. In this earlier essay, however, Keynes distinguished between unemployment caused by temporary economic breakdowns and what he called "technological unemployment" – that is, "unemployment due to the discovery of means of economising the use of labour outrunning the pace at which we can find new uses for labour".

Keynes reckoned that we would hear much more about this kind of unemployment in the future. But its emergence, he thought, was a cause for hope, rather than despair. For it showed that the developed world, at least, was on track to solving the "economic problem" – the problem of scarcity that kept mankind tethered to a burdensome life of toil.

Machines were rapidly replacing human labour, holding out the prospect of vastly increased production at a fraction of the existing human effort. In fact, Keynes thought that by about now (the early 21st century) most people would have to work only 15 hours a week to produce all that they needed for subsistence and comfort.

Developed countries are now about as rich as Keynes thought they would be, but most of us work much longer than 15 hours a week, although we do take longer holidays, and work has become less physically demanding, so we also live longer. But, in broad terms, the prophecy of vastly increased leisure for all has not been fulfilled. Automation has been proceeding apace, but most of us who work still put in an average of 40 hours a week. In fact, working hours have not fallen since the early 1980s.

At the same time, "technological unemployment" has risen. Since the 1980s, we have never regained the full employment levels of the 1950s and 1960s. If most people still work a 40-hour week, a substantial and growing minority have had unwanted leisure thrust upon them in the form of unemployment, under-employment and forced withdrawal from the labour market. And, as we recover from the current recession, most experts expect this group to grow even larger.

What this means is that we have largely failed to convert growing technological unemployment into increased voluntary leisure. The main reason for this is that the lion's share of the productivity gains achieved over the last 30 years has been seized by the well-off.

Particularly in the United States and Britain since the 1980s, we have witnessed a return to the capitalism "red in tooth and claw" depicted by Karl Marx. The rich and very rich have become very much richer, while everyone else's incomes have stagnated. So most people are not, in fact, four or five times better off than they were in 1930. It is not surprising that they are working longer than Keynes thought they would.

But there is something else. Modern capitalism inflames, through every sense and pore, the hunger for consumption. Satisfying that hunger has become the great palliative of modern society, our counterfeit reward for working irrational hours. Advertisers proclaim a single message: your soul is to be discovered in your shopping.

Aristotle knew of insatiability only as a personal vice; he had no inkling of the collective, politically orchestrated insatiability that we call economic growth. The civilization of "always more" would have struck him as moral and political madness.

And, beyond a certain point, it is also economic madness. This is not just or mainly because we will soon enough run up against the natural limits to growth. It is because we cannot go on for much longer economising on labour faster than we can find new uses for it. That road leads to a division of society into a minority of producers, professionals, supervisors, and financial speculators on one side, and a majority of drones and unemployables on the other.

Apart from its moral implications, such a society would face a classic dilemma: how to reconcile the relentless pressure to consume with stagnant earnings. So far, the answer has been to borrow, leading to today's massive debt overhangs in advanced economies. Obviously, this is unsustainable, and thus is no answer at all, for it implies periodic collapse of the wealth-producing machine.

The truth is that we cannot go on successfully automating our production without rethinking our attitudes toward consumption, work, leisure, and the distribution of income. Without such efforts of social imagination, recovery from the current crisis will simply be a prelude to more shattering calamities in the future.

Source: Guardian - Return to capitalism 'red in tooth and claw' spells economic madness

The Sensory Effect | Ray Kurzweil

Ray Kurzweil delivers "The Sensory Effect" keynote speech at the NY Tech Meetup. Ray talks about exponential growth, the role that information systems will play in the future of healthcare, artificial intelligence and additional topics.

Ray Kurzweil - "The Sensory Effect"

Ray Kurzweil - "The Sensory Effect"

The 100,000-Student Classroom | Peter Norvig [TED]

In the fall of 2011 Peter Norvig taught a class with Sebastian Thrun on artificial intelligence at Stanford attended by 175 students in situ -- and over 100,000 via an interactive webcast. He shares what he learned about teaching to a global classroom.

Peter Norvig: The 100,000-student classroom

Peter Norvig: The 100,000-student classroom

Thursday, June 21, 2012

A Date with History: 17 yr old Brittany Trilford Addresses World Leaders at the UN Earth Summit

Brittany Trilford Speech to UN Rio+20 Summit Opening Ceremony

Tena Koutou from New Zealand. My name is Brittany Trilford. I am seventeen years old, a child. Today, in this moment, I am all children, your children, the world’s three billion children. Think of me for these short minutes as half the world.

I stand here with fire in my heart. I’m confused and angry at the state of the world and I want us to work together now to change this. We are here to solve the problems that we have caused as a collective, to ensure that we have a future.

You and your governments have promised to reduce poverty and sustain our environment. You have already promised to combat climate change, ensure clean water and food security. Multi-national corporations have already pledged to respect the environment, green their production, compensate for their pollution. These promises have been made and yet, still, our future is in danger.

We are all aware that time is ticking and is quickly running out. You have 72 hours to decide the fate of your children, my children, my children’s children. And I start the clock now… tck tck tck.

Let us think back to twenty years ago - well before I was even an inkling in my parents’ eyes - back to here, to Rio, where people met at the first Earth Summit in 1992. People at this Summit knew there needed to be change. All of our systems were failing and collapsing around us. These people came together to acknowledge these challenges to work for something better, commit to something better.

They made great promises, promises that, when I read them, still leave me feeling hopeful. These promises are left – not broken, but empty. How can that be? When all around us is the knowledge that offers us solutions. Nature as a design tool offers insight into systems that are whole, complete, that give life, create value, allow

progress, transformation, change.

We, the next generation, demand change. We demand action so that we have a future and have it guaranteed. We trust that you will, in the next 72 hours, put our interests ahead of all other interests and boldly do the right thing. Please, lead. I want leaders who lead.

I am here to fight for my future. That is why I’m here. I would like to end by asking you to consider why you’re here and what you can do. Are you here to save face? Or are you here to save us?

A Date with History: 17 yr old Brittany Trilford addresses world leaders at the UN Earth Summit

Tena Koutou from New Zealand. My name is Brittany Trilford. I am seventeen years old, a child. Today, in this moment, I am all children, your children, the world’s three billion children. Think of me for these short minutes as half the world.

I stand here with fire in my heart. I’m confused and angry at the state of the world and I want us to work together now to change this. We are here to solve the problems that we have caused as a collective, to ensure that we have a future.

You and your governments have promised to reduce poverty and sustain our environment. You have already promised to combat climate change, ensure clean water and food security. Multi-national corporations have already pledged to respect the environment, green their production, compensate for their pollution. These promises have been made and yet, still, our future is in danger.

We are all aware that time is ticking and is quickly running out. You have 72 hours to decide the fate of your children, my children, my children’s children. And I start the clock now… tck tck tck.

Let us think back to twenty years ago - well before I was even an inkling in my parents’ eyes - back to here, to Rio, where people met at the first Earth Summit in 1992. People at this Summit knew there needed to be change. All of our systems were failing and collapsing around us. These people came together to acknowledge these challenges to work for something better, commit to something better.

They made great promises, promises that, when I read them, still leave me feeling hopeful. These promises are left – not broken, but empty. How can that be? When all around us is the knowledge that offers us solutions. Nature as a design tool offers insight into systems that are whole, complete, that give life, create value, allow

progress, transformation, change.

We, the next generation, demand change. We demand action so that we have a future and have it guaranteed. We trust that you will, in the next 72 hours, put our interests ahead of all other interests and boldly do the right thing. Please, lead. I want leaders who lead.

I am here to fight for my future. That is why I’m here. I would like to end by asking you to consider why you’re here and what you can do. Are you here to save face? Or are you here to save us?

A Date with History: 17 yr old Brittany Trilford addresses world leaders at the UN Earth Summit

Organisms as Applications | Andrew Hessel | Synthetic Biology

Presentación de Andrew Hessel en el seminario "Tecnologías exponenciales para resolver los grandes problemas de la humanidad" desarrollado por el Centro de Innovación TECHO y Movistar Innova en Marzo de 2012.

Presentación de Andrew Hessel en Seminario CI-Movistar Innova

Presentación de Andrew Hessel en Seminario CI-Movistar Innova

Incredibly Young and Smart Entrepreneurs Aiming for the Moonshot | 20 Under 20 | Thiel Fellowship

The dropouts, the misfits and wunkerkinds. The young and the fearless. They come every year to Silicon Valley. And mostly, they have come on their own.

It wasn’t until last year there that was a dedicated program for them. The famously contrarian and libertarian investor Peter Thiel created a fellowship for twenty people under the age of 20. The mission was to find uncommonly brilliant young people and get them to forgo the traditional path of college. The first class went on to start companies, raise several million dollars in venture capital or work on complex technical problems in biology.

Now Thiel’s foundation is on its second year. What the foundation looks for actually hasn’t changed all that much, the foundation’s co-founder Jim O’Neill tells us. The application form still has Thiel’s very famous interview question, which probes for a person’s capacity to think independently. He asks, “Tell us something about the world that you think is true that most people think is not true.”

There is also another variant of this question later on, which asks: “What is one thing that exists today that you would like to make absurd in 20 years?”

“We’re looking for intellectual independence and a determination to make something new and to make it work,” O’Neill says.

Some of fellows are exactly what you would expect — if anything predictable could ever come out of this program. There is the youngest person to have ever created nuclear fusion, Taylor Wilson. (An excellent story about him from Popular Science is right here.)

There is also a pair that’s working on biomedical imaging with the vision that it could one day be precise enough to spot as few as 10 cancer cells.

“Doctors often use mainly qualitative information in diagnosing disease,” Anand Gupta said in a presentation at the San Francisco Palace of the Fine Arts earlier this year. “Biomedical imaging has the density, structure and information to provide more rational tools to find disease.”

Yet another fellow, Harvard student Connor Zwick, has an iPhone app that makes enough to bring him a livable income. It’s a Flashcards app, which seems simple at the surface level. But he thinks about it as a learning network that responds and adapts to how people progress with intaking new material.

Another fellow Chris Olah got hooked on 3D printing when he was a teenager spending time at Toronto’s Hack Lab. He had already dropped out of college.

“The time obligations of university made it difficult to work on projects that I wanted to pursue,” he said in an interview. “There are only so many hours in a day.”

Some of the projects can easily be turned into consumer web startups, while others are more research-oriented. Some problems the fellows are attacking can be solved by brute technical force, while others are far more political like health care. Ilya Vakhutinsky, for example, is trying to automate home care after working on data visualization at a plasma physics laboratory.

Even though Thiel believes that we may be in a “higher education bubble,” there aren’t any plans to scale the fellowship beyond 20 people a year. O’Neill says it should inspire others to take the same leap in thinking critically about whether they need a university degree or not.

Here are the fellows:

Clay Allsopp (20, Raleigh, NC) thinks people should be able to forget about technology and simply focus on being creative. His start-up, Apptory, helps individuals and businesses create and distribute content for touch-screen devices, using an intuitive, easy-to-understand interface.

Dylan Field (20, Penngrove, CA) envisions a world where people define themselves by what they create rather than what they consume. Currently stopped out of Brown University, Field is working with his former classmate Evan Wallace on making better creative tools.

Kettner Griswold (19, Bethesda, MD) and Paul Sebexen (19, Staten Island, NY) are stopping out of school to work on a benchtop genome synthesis device, which will allow individual laboratories and medical practices to synthesize large genetic constructs in-house for an unprecedented low recurring cost. This product would massively disrupt the fields of biotechnology and health care, fueling innovation and stimulating interest and research sector-wide.

Anand Gupta (20, Palo Alto, CA) and Tony Ho (19, San Jose, CA) are using their expertise in biology and computer science to transform the way doctors diagnose patients. Their service will enable doctors and researchers to receive quantitative analysis of biomedical images, allowing for faster, more accurate diagnoses of complex diseases – and more lives saved.

Spencer Hewett (20, Bryan Mawr, PA) has an insatiable passion for inventing that extends far beyond the confines of one particular industry. As a Thiel fellow, he will focus on No-Q, a fusion of radio-frequency identification (RFID) and mobile payment technology that will eliminate both checkout lines and shoplifting.

Yoonseo Kang (18, Mississauga, ON, Canada) recognizes that society’s potential for innovation and abundance can only be achieved if knowledge and the factors of production are accessible for everyone. With that in mind, Yoonseo sees open-source hardware as the key for enabling communities around the world to vastly increase their productive potential and together engage in strategic economic collaboration. To that end, he is working with Open Source Ecology to develop the Global Village Construction Set, the 50 industrial machines that it takes to build a civilization with modern comforts.

Jimmy Koppel (20, St. Louis, MO) has a passion for software engineering – and a plan to make it much more efficient. Modifying software today often involves hundreds of thousands of small, similar adjustments that require a great deal of time and money. James will fix that problem by developing new tools to automate the process.

Ryan Lelek (19, Schererville, IN) developed a passion for entrepreneurship at the age of 15, when he established his first “instant streaming” start-up. Now he’s dedicated to disrupting the computer industry, using new advances in hardware, software, and network technology. As a Thiel Fellow, he’ll continue to change the world by creating simple technology tools that empower people.

Ritik Malhotra (19, San Jose, CA) Ritik began programming at age 8; started a popular web forum at the age of 12 that grew to over 32,000 members; and ran a web hosting and software consultancy business at the age of 13, garnering over a 600x return on his initial investment. Now he wants to provide a streamlined way of discovering, sharing, and distributing content over Facebook, Twitter, and other social media services. As a Thiel Fellow, he’ll first work to build a service that allows users to share interesting media, scraped from all around the web, focusing primarily on user growth in order to build a thriving community.

Chris Olah (19, Toronto, ON, Canada) wants to use 3D printing to reduce the scope of scarcity. His goal: empower anyone with a 3D printer to make educational aids, basic scientific equipment, and tools that improve their quality of life. He is currently working on a project called ImplicitCAD, which is a math-based attempt to reinvent computer-aided design and make it more affordable.

Semon Rezchikov (18, Hillsborough, NJ) is eager to explore how synthetic biology, nanotechnology, and social network dynamics intersect. As a Thiel Fellow, he wants to develop more flexible bioautomation technologies to improve the design cycle speed, and then use those technologies to create a library of truly reliable parts – making synthetic biology more like engineering and less like science.

Omar Rizwan (18, East Hanover, NJ) wants to change the world through the control and analysis of information. Specifically, he plans to speed up progress in the field of artificial intelligence by working on the analysis of big data sets. He will aggregate large sets of data from many different Internet sources and use them to tease out trends and draw conclusions.

Tara Seshan (19, New Fairfield, CT) is dedicated to improving public health worldwide, using technology, simple solutions, and community-based change. To that end, she is developing a tool that influences analysis of data, monitoring and evaluation, and public health decision making. As a Thiel Fellow, Tara will explore developing tools that enhance public health programs that can be implemented in low-resource settings.

Noor Siddiqui (17, Clifton, VA) is inspired to galvanize people for the good of others. As a Thiel Fellow, she will work to give students across the globe access to upward mobility – and industries access to an untapped work force – with the goal of mobilizing one billion people in the next decade.

Charlie Stigler (19, Pacific Palisades, CA) has years of experience as an entrepreneur and engineer, having written the popular open-source study application, SelfControl, and founded two Web start-ups. Now he’s working on Zaption, an application that improves the usual workflow for educators and collaborators by allowing video to be integrated into interactive Web experiences and studies. He believes this technology can help solve fundamental problems, starting with that of the U.S. education system.

Ilya Vakhutinsky (20, Fair Lawn, NJ) wants to revolutionize the way the technology and health care communities work together. He is working to create a more open and transparent health care system, drastically lowering the cost of care and empowering patients to make better decisions.

Taylor Wilson (18, Texarkana, AR) became the youngest person in history to create nuclear fusion. Since then, he has produced the lowest-cost and lowest-dose active interrogation system for the detection of enriched uranium ever developed. As a Thiel Fellow, Taylor will focus on both counter-terrorism and the production of medical isotopes for use in the diagnosis and treatment of cancer.

Connor Zwick (18, Waukesha, WI) is passionate about education – which is why he has set out to revolutionize our country’s antiquated system using technology. As a Thiel Fellow, he will focus on Flashcards+, a mobile educational platform with a base of over 1.5 million downloads that allows anyone to learn anything using crowd sourced generated content from a database of more than 400 million flashcards.

Source: Nuclear Fusion, 3D Printing, Biomedical Imaging: What Thiel’s New 20 Under 20 Fellows Are Attacking

Read also: What Happened to the Future? by Bruce Gibney | Founders Fund

Wednesday, June 20, 2012

MUST WATCH! THRIVE: What On Earth Will It Take?

THRIVE is an unconventional documentary that lifts the veil on what's REALLY going on in our world by following the money upstream -- uncovering the global consolidation of power in nearly every aspect of our lives. Weaving together breakthroughs in science, consciousness and activism, THRIVE offers real solutions, empowering us with unprecedented and bold strategies for reclaiming our lives and our future.

Visit: Thrive

THRIVE: What On Earth Will It Take?

Visit: Thrive

THRIVE: What On Earth Will It Take?

Saturday, June 16, 2012

What Money Can't Buy - The Moral Limit of Markets | London School of Economics

Speaker: Professor Michael Sandel

Discussants: Stephanie Flanders, Professor Julian Le Grand, Rt Revd Peter Selby

Chair: Ann Pettifor

Recorded on 23 May 2012 in St Paul's Cathedral, London.

Is there something wrong with a world in which everything is for sale? If so, how can we prevent market values from reaching into spheres of life where they don't belong? What are the moral limits of markets?

Noted public philosopher and Harvard professor Michael J. Sandel will explore some of these pressing questions with responses from Stephanie Flanders, Professor Julian Le Grand and Bishop Peter Selby. St Paul's Cathedral is delighted to host a discussion on this vital topic within a sacred space in order to explore the intersection between faith, morality and markets and the power that money has in our lives. Questions and comments from the audience will be taken.

Michael J. Sandel is the Anne T. and Robert M. Bass Professor of Government at Harvard University, where he has taught political philosophy since 1980. His recent book, Justice: What's the Right Thing to Do? relates the big questions of political philosophy to the most vexing issues of our time. His new book, What Money Can't Buy: The Moral Limits of Markets, has just been published. At Harvard, Sandel's courses include Ethics, Biotechnology, and the Future of Human Nature, Ethics, Economics, and Law, and Globalization and Its Critics. His undergraduate course, Justice, has enrolled over 15,000 students, and is the first Harvard course to be made freely available online and on public television. A recipient of the Harvard-Radcliffe Phi Beta Kappa Teaching Prize, Sandel was recognised by the American Political Science Association in 2008 for a career of excellence in teaching. He has been a visiting professor at the Sorbonne (Paris), delivered the Tanner Lectures on Human Values at Oxford University, and in 2009 delivered the BBC Reith Lectures. In 2010, China Newsweek named him the "most influential foreign figure of the year" in China.

Stephanie Flanders has been a reporter at the New York Times (2001); a speech writer and senior advisor to the US Treasury Secretary (1997-2001); a Financial Times leader-writer and columnist (1993-7); and an economist at the Institute for Fiscal Studies and London Business School. She became BBC economics editor in April 2008. She has won numerous awards, including the 2010 Harold Wincott Award for online journalism. She blogs at Stephanomics.

Julian Le Grand is the Richard Titmuss Professor of Social Policy at the London School of Economics. He is an Honorary Fellow of the Faculty of Public Health Medicine, a Trustee of the Kings Fund, and a Founding Academician of the Academy of Learned Societies for the Social Sciences. He has an honorary doctorate from the University of Sussex. In 2003-5 he was seconded to No 10 Downing St as a senior policy adviser to the Prime Minister. As well as his position at No 10, he has acted as an adviser to the President of the European Commission, the World Bank, the World Health Organisation, the OECD, Her Majesty's Treasury and the UK Departments of Health and Work and Pensions.

Dr Peter Selby was Bishop of Worcester from 1997 until 2007 and in 2001 was also appointed to Bishop of Prisons, a post from which he also retired in September 2007. Dr Selby's interest in prisons is long-standing, and he is himself the son of refugees, and served for a time as the Chair of the Asylum Committee of the Refugee Council. His concern for prisons and the criminal justice system extends back to 1965 when he served as an interim chaplain at San Quentin, California, as part of his ministerial training.

Ann Pettifor is director of Policy Research in Macro-Economics (PriME), and a senior fellow of the New Economics Foundation. She is the author of The Coming First World Debt Crisis which was published in 2006

What Money Can't Buy - the moral limit of markets

Discussants: Stephanie Flanders, Professor Julian Le Grand, Rt Revd Peter Selby

Chair: Ann Pettifor

Recorded on 23 May 2012 in St Paul's Cathedral, London.

Is there something wrong with a world in which everything is for sale? If so, how can we prevent market values from reaching into spheres of life where they don't belong? What are the moral limits of markets?

Noted public philosopher and Harvard professor Michael J. Sandel will explore some of these pressing questions with responses from Stephanie Flanders, Professor Julian Le Grand and Bishop Peter Selby. St Paul's Cathedral is delighted to host a discussion on this vital topic within a sacred space in order to explore the intersection between faith, morality and markets and the power that money has in our lives. Questions and comments from the audience will be taken.

Michael J. Sandel is the Anne T. and Robert M. Bass Professor of Government at Harvard University, where he has taught political philosophy since 1980. His recent book, Justice: What's the Right Thing to Do? relates the big questions of political philosophy to the most vexing issues of our time. His new book, What Money Can't Buy: The Moral Limits of Markets, has just been published. At Harvard, Sandel's courses include Ethics, Biotechnology, and the Future of Human Nature, Ethics, Economics, and Law, and Globalization and Its Critics. His undergraduate course, Justice, has enrolled over 15,000 students, and is the first Harvard course to be made freely available online and on public television. A recipient of the Harvard-Radcliffe Phi Beta Kappa Teaching Prize, Sandel was recognised by the American Political Science Association in 2008 for a career of excellence in teaching. He has been a visiting professor at the Sorbonne (Paris), delivered the Tanner Lectures on Human Values at Oxford University, and in 2009 delivered the BBC Reith Lectures. In 2010, China Newsweek named him the "most influential foreign figure of the year" in China.

Stephanie Flanders has been a reporter at the New York Times (2001); a speech writer and senior advisor to the US Treasury Secretary (1997-2001); a Financial Times leader-writer and columnist (1993-7); and an economist at the Institute for Fiscal Studies and London Business School. She became BBC economics editor in April 2008. She has won numerous awards, including the 2010 Harold Wincott Award for online journalism. She blogs at Stephanomics.

Julian Le Grand is the Richard Titmuss Professor of Social Policy at the London School of Economics. He is an Honorary Fellow of the Faculty of Public Health Medicine, a Trustee of the Kings Fund, and a Founding Academician of the Academy of Learned Societies for the Social Sciences. He has an honorary doctorate from the University of Sussex. In 2003-5 he was seconded to No 10 Downing St as a senior policy adviser to the Prime Minister. As well as his position at No 10, he has acted as an adviser to the President of the European Commission, the World Bank, the World Health Organisation, the OECD, Her Majesty's Treasury and the UK Departments of Health and Work and Pensions.

Dr Peter Selby was Bishop of Worcester from 1997 until 2007 and in 2001 was also appointed to Bishop of Prisons, a post from which he also retired in September 2007. Dr Selby's interest in prisons is long-standing, and he is himself the son of refugees, and served for a time as the Chair of the Asylum Committee of the Refugee Council. His concern for prisons and the criminal justice system extends back to 1965 when he served as an interim chaplain at San Quentin, California, as part of his ministerial training.

Ann Pettifor is director of Policy Research in Macro-Economics (PriME), and a senior fellow of the New Economics Foundation. She is the author of The Coming First World Debt Crisis which was published in 2006

What Money Can't Buy - the moral limit of markets

Tuesday, June 12, 2012

The Integrated Circuit of Biology | Stephen Quake [TEDx]

Stephen Quake studied physics (BS '91) and mathematics (MS '91) at Stanford University before earning his doctorate in physics from Oxford University as a Marshall scholar ('94). Thereafter, as a postdoc in Nobel Laureate Steven Chu's group at Stanford, he developed techniques to manipulate single DNA molecules with optical tweezers. In 1996 Steve joined the faculty of Caltech, where he was ultimately appointed Thomas and Doris Everhart Professor of Applied Physics and Physics. In 2004 he returned to Stanford to help launch a new Department of Bioengineering, where he is the Lee Otterson Professor and co-chair. Steve has received "Career" and "First" awards from the National Science Foundation and National Institutes of Health (NIH), was a Packard Fellow, was awarded an NIH Director's Pioneer Award, and is an investigator of the Howard Hughes Medical Institute. He is a founder and scientific advisory board chair of Fluidigm, Inc. and Helicos Biosciences, Inc.

TEDxCaltech - Stephen Quake - The Integrated Circuit of Biology

TEDxCaltech - Stephen Quake - The Integrated Circuit of Biology

Saturday, June 9, 2012

MUST READ! John Maynard Keynes: A Vision for the Future or a Ghost from the Past?

(This paper was presented as the keynote address at the Seventh Annual Moral Foundations of Capitalism Conference hosted by the Clemson Institute for the Study of Capitalism in Clemson, South Carolina, on May 30, 2012)

The current economic crisis that has engulfed the United States and much of the rest of the world over the last few years, has seen a dramatic revival in the economic ideas and policy prescriptions of the most famous British economist of the 20th century, John Maynard Keynes. This has seemed surprising to some, since it was presumed that traditional Keynesian Economics was more or less relegated (to use Karl Marx's phrase) to "the dustbin of history."

After dominating the economics profession for more than a quarter of a century following the Second World War, Keynesianism had been challenged by various "counter-revolutions" in Macroeconomics beginning in the late 1960s and 1970s. They had taken the forms of Monetarism, Supply-Side Economics, New Classical or Rational Expectations Theory, New Keynesianism, and even Austrian Economics, following the awarding of the Nobel Prize to F. A. Hayek in the 1974.

The fact is, however, that neither Keynes nor his economics have ever been gone or replaced. Keynesian Economics has continued to dominate and hold sway over the way the vast majority of economists think about and analyze the nature of economy-wide fluctuations in employment and output.

The Legacy of Keynes's "Demand Management" Economics

It is the idea that government must manage and guide monetary and fiscal policy to assure full employment, a stable price level and to foster economic growth. Some of the terms of the debate may have changed over the last half-century or so, but the belief that it is the responsibility of government to control the supply of money and aggregate spending in the economy persist-s today just as much as it did in the 1940s.

The modern conception of "demand management" is a legacy of John Maynard Keynes's 1936 book The General Theory of Employment, Interest and Money. The impact of Keynes's book and its message should not be underestimated. Its two central tenets are the claim that the market economy is inherently unstable and likely to generate prolonged periods of unemployment and underutilized productive capacity, and the argument that governments should take responsibility to counteract these periods of economic depression with the various monetary and fiscal policy tools at their disposal. This was bolstered by Keynes's belief that policy managers guided by the economic theory developed in his book could have the knowledge and ability to do so successfully.

No less important in propagating his idea of demand management economic policy was Keynes's literary ability to persuade. As Leland Yeager expressed it, "Keynes saw and provided what would gain attention − harsh polemics, sardonic passages, bits of esoteric and shocking doctrine." Keynes possessed an arrogant amount of self-confidence and belief in his ability to influence public opinion and policy.

Austrian economist Friedrich A. Hayek, who knew Keynes fairly well, referred to his "supreme confidence . . . in his power to play on public opinion as a supreme master plays his instrument." On the last occasion he saw Keynes in early 1946 (shortly before Keynes' death from a heart attack), Hayek asked him if he wasn't concerned that some of his followers were taking his ideas to extremes. Keynes replied that Hayek did not need to be worried. If it became necessary, Hayek could "rely upon him again quickly to swing round pubic opinion—and he indicated by a quick movement of his hand how rapidly that would be done. But three months later he was dead."

Even today, respected economists argue that Keynesian-style macroeconomic intervention is needed as a balancing rod against instability in the market economy. One example is Robert Skidelsky, the author of a widely acclaimed multi-volume biography of Keynes and the recently published, Keynes: The Return of the Master (2009)?.

A few years ago Professor Skidelsky argued that capitalism has at its heart an instability of financial institutions and, "This insight by Keynes into the causes and consequences of financial crises remains supremely valuable." In any significant economic downturn, government should begin "pumping money into the economy, like pumping air into a deflating balloon."

Keynes first established his reputation as a public figure in the immediate aftermath of the First World War. During war, he had worked in the British Treasury. In 1919 he served as an adviser to the British delegation in Versailles. But frustrated with the attitude of the Allied powers toward Germany in setting the terms of the peace, Keynes returned to Britain and published The Economic Consequences of the Peace, in which he severely criticized the peace settlement.

In 1923, he published A Tract on Monetary Reform, in which he called for the end of the gold standard, suggesting a national man-aged paper currency in its place. He strongly opposed Great Britain's return to the gold standard in the mid-1920s at the prewar gold parity. He argued that governments should have discretionary power over the management of a nation's monetary system to as-sure a desired target level of employment, output, and prices.

In 1930 Keynes published A Treatise on Money, a two-volume work that he hoped would establish his reputation as a leading monetary theorist of his time instead of only an influential economic policy analyst. However, over the next two years a series of critical reviews appeared, written by some of the most respected economists of the day. The majority of them demonstrated serious problems with either the premises or the reasoning with which Keynes attempted to build his theory on the relationships between savings, investment, the interest rate, and the aggregate levels of output and prices. But the most devastating criticisms were made by a young Friedrich A. Hayek in a two-part review essay that appeared in 1931-1932.

Hayek argued that Keynes seemed to understood neither the nature of a market economy in general nor the significance and role of the rate of interest in maintaining a proper balance between savings and investment for economic stability. At the most fundamental level Hayek argued that Keynes's method of aggregating the individual supplies and demands for a multitude of goods into a small number of macroeconomic "totals" distorted any real understanding of the relative price and production relationships in and between actual markets. "Mr. Keynes's aggregates conceal the most fundamental mechanisms of change," Hayek said.

Keynes devoted the next five years to reconstructing his argument, the re-sult being his most famous and influential work, The General Theory of Employment, Interest and Money, published in 1936.

Keynes argued that the Great Depression was caused by inescapable irrationalities in the market economy that not only created the conditions for the severity of the economic downturn, but necessitated activist monetary and fiscal policies by government to restore and maintain full employment and maximum utilization of resource and output capabilities. For the next half-century Keynes's ideas, as presented in The General Theory, became the cornerstone of macroeconomic theorizing and policy-making throughout the Western world, and continue to dominate public policy thinking today.

John Maynard Keynes and the "New Liberalism"

What where the wider philosophical principles and ideas behind Keynes views about a market society? In 1925, John Maynard Keynes delivered a lecture at Cambridge titled "Am I a Liberal?" He rejected any thought of considering himself a conservative because conservatism "leads nowhere; it satisfies no ideal; it conforms to no intellectual standard; it is not even safe, or calculated to preserve from spoilers that degree of civilization which we have already attained."

Keynes then asked whether he should consider joining the Labor Party. He admitted, "Superficially that is more attractive," but rejected it as well. "To begin with, it is a class party, and the class is not my class," Keynes argued. Furthermore, he doubted the intellectual ability of those controlling the Labor Party, believing that it was dominated by "those who do not know at all what they are talking about."

This led Keynes to conclude that all things considered, "the Liberal Party is still the best instrument of future progress—if only it has strong leadership and the right program." But the Liberal Party of Great Britain could serve a positive role in society only if it gave up "old-fashioned individualism and laissez-faire," which he considered "the dead-wood of the past." Instead, what was needed was a "New Liberalism" that would involve "new wisdom for a new age." What this entailed, in Keynes's view, was "the transition from economic anarchy to a regime which deliberately aims at control-ling and directing economic forces in the interests of social justice and social stability."